Survey Says: Consumers are Increasingly Using GenAI for Shopping...

Morgan Stanley's quarterly report shows overall GenAI usage rising rapidly, Gemini on the rise, and consumers are using GenAI for

Sunday night, Morgan Stanley, released their Q1 ‘Alphawise’ consumer survey. In the survey they’ve been asking a panel of consumers about their GenAI usage and underlying behaviors that is very applicable to where we think things are going here at Retailgentic.

Let’s dig in!

About Morgan Stanley Alphawise

Before we get deep into the data, here’s a blurb about the survey methodology from Morgan Stanley.

Note that I’m aware of the arguments against surveys (glances sideways at Jason Goldberg), and I get that stated preference is different than observed/measured actions. Even if you don’t love survey data, the consistency of the MS survey at a minimum gives directional data about where consumers are moving.

The other aspect of the survey to be aware of - the survey has three buckets of demographics by age group that don’t track the usual gen alpha/gen z/millennial/Gen X, etc. They are 16-24, 25-34, 35+.

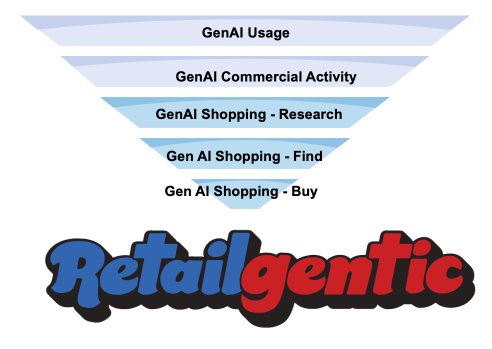

Introducing the Retailgentic GenAI Shopping Agent Adoption Funnel

Our overall thesis here at Retailgentic is that we are at the beginning of a major change in how people shop online. We believe shopping agents are going to be one of the fastest and most disruptive changes to hit retail and ecommerce since the founding of Amazon. Big changes come in a series of connected small steps, and we’ve identified the five sub-steps that will help us track where we are in the Retailgentic adoption curve. This is built off our experience at the early days of the search, e-commerce, marketplace and mobile changes that all went through similar stages.

Retailgentic Adoption Funnel

With any new model, the ultimate 'it’s here’ moment will be when 50% of sales come from agents. We’re starting at basically 0 right now, but we’re going to start tracking these over time to watch the acceleration to 50%.

GenAI Usage - At the top of the funnel, consumers need to engage with the various GenAI engines. At this level, consumers are doing research, homework and generally using the GenAI innovative capabilities.

GenAI Commercial activity - Within that top-of-funnel GenAI usage a % of that activity is going to be ‘commercial’ activity - the consumer isn’t doing purely informational searches and conversations, they are performing commercial activity. Commercial activity is any purchase intent - it could be a car, service, travel and even ecommerce or online shopping.

GenAI Shopping - Research - A portion of that commercial activity will be online shopping and the first thing consumers do with a new experience like GenAI is use it to research. The research / discovery process of shopping is somewhat broken, and GenAI is especially good at research, so this is a great opportunity to show consumers the benefits GenAI has to offer for online shopping.

GenAI Shopping - Find - After research, consumers are going to compare some features and do price comparisons to narrow down the universe of products down to 2-4 items to buy (SKUs). This is the Find cycle.

Gen AI Shopping - Buy - Finally at the bottom of the funnel, we have the purchase. At this point the consumer is looking at final considerations like payment options, local availability, BOPIS, shipping costs and times before they hit the agentic ‘buy button’.

With that framework in mind, let’s get a read for where we are.

Overall GenAI Usage

The first data in Exhibit 1, shows the huge growth of usage across the three top GenAI engines: ChatGPT, Google Gemini and Meta AI. Here you can see that Gemini led the growth pack with a 5.5% increase over six months. Meta had a strong showing at 2.4% while ChatGPT grew share 1.89%.

What’s interesting at this top-level is that all three rose indicating they are not taking existing share, but they are fighting over ‘new share’. This shows us that we are still early days and so many consumers continue to flood in that the GenAI companies are adding more and more customers, in some examples, moving consumers over from a old-school business model (e.g. Google traditional search→ Gemini).

Reported MAU/DAUs

Those are growth rates, but where are we in terms of scale? Our friends at Morgan Stanley, have conveniently provided this chart. In this chart, the Metrics are:

DAU - Daily Active Users (user was active in last 24hrs)

WAU - Weekly Active Users (user was active in last 7 days)

MAU - Monthly Active Users (user was active in last 30 days)

Game theory tells us that if you are doing well, you want to hide it. Also, if you are doing poorly, you also want to hide it. Therefore, It’s impossible for us to know why, for example, ChatGPT is only releasing WAUs- some would argue their DAU must be much lower (implying not a lot of regular usage). Or…could it be they are hiding DAI because it’s high?

For example, look at the Gemini MAU/DAU delta and the same for Perplexity - that’s a big drop off.

Adding these together at the MAU level we get: 500+1000+350+30=1,880 - call it 2b global users. Here I imagine the US is heavy for chatgpt and gemini, at say 40%, but light for meta given that the bulk of Whatsapp users are non domestic.

There are ~330m US consumers, this indicates we’re at 40% * 880m = 352m, but there’s a lot of early adopters using multiple engines - so I’d give this a 50% haircut so call it 176m or about half the US population is using one of the engines at least monthly.

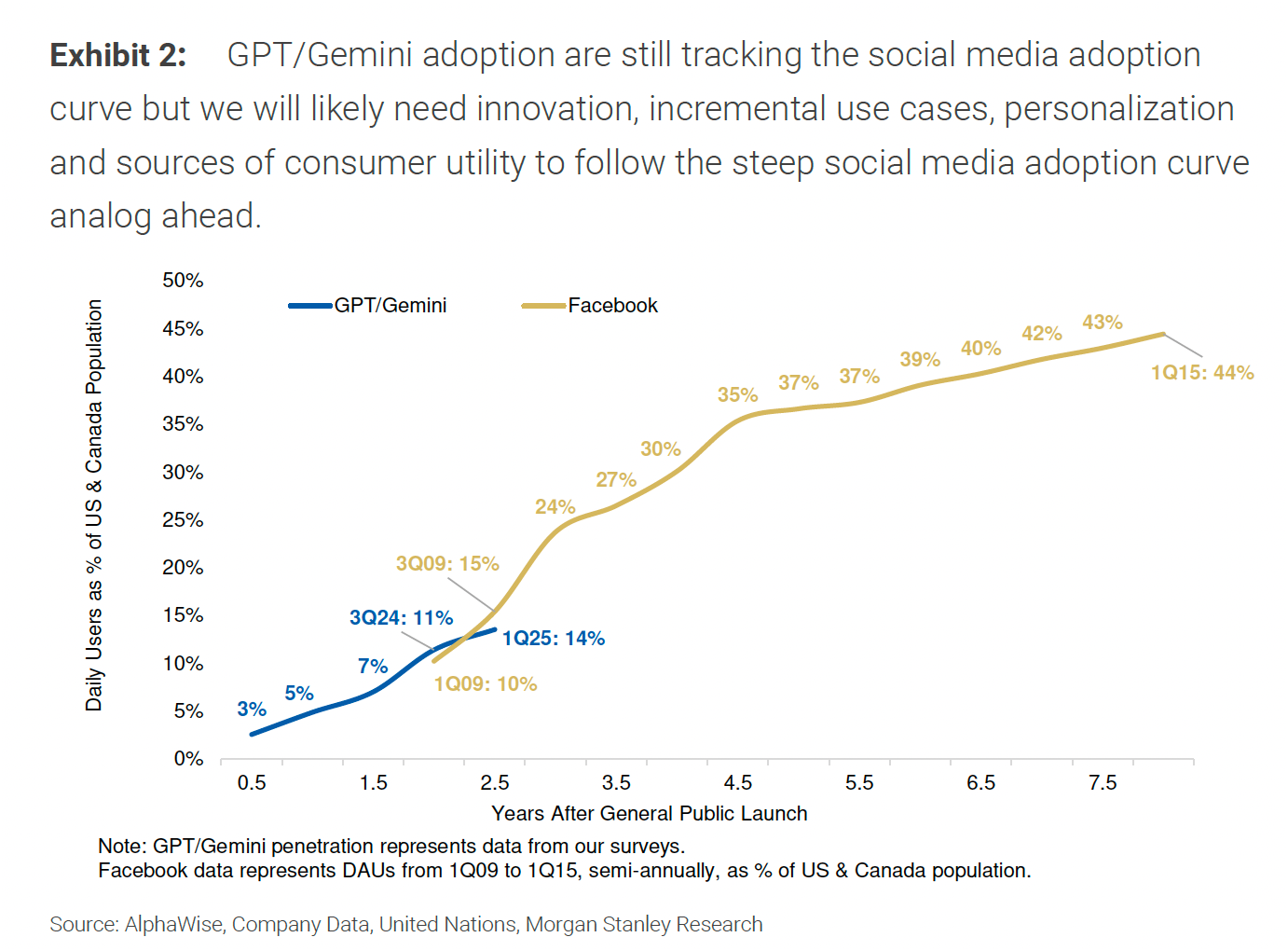

GenAI vs. Facebook/Social Growth Curves

Another interesting analysis MS does is they line up the adoption curve as % of US+CA population for Facebook and ‘index’ it to where we are for ChatGPT+Gemini.

You’ll see they are tracking a very similar slope, but GenAI has a big hurdle this year- going from 14% to 24% which is a huge adoption surge. We’re at the start of ‘new model and release’ season so in May/June we should see a lot of innovation that can keep the growth rolling.

Peeling the onion by age cohort…

Gemini’s growth is particularly strong and in Exhibits 3 and 4, the same data from Exhibit 1 is sliced by age group. Exhibit 3 is the 16-24 age group and Exhibit 4 is 25-34.

What’s interesting here is:

16-24 year olds - ChatGPT won the day in this age group at a 12% increase, followed by Gemini at 4.6% and Meta AI lagged by 1%. This may indicate the younger cohort doesn’t use the Meta AI product with AI which is WhatsApp.

25-34 year olds - Gemini won this group growing a whopping 16% with ChatGPT growing ~9% and finally we see an age group that grew with Meta - up ~8%.

That’s a good summary of the top of the funnel, GenAI Usage, and what’s going on. Now let’s go down a level to see how much of that is informational behavior and how much is commercial.

GenAI Commercial Use

Since MS started tracking the GenAI data in the survey (only 2023 I believe), the commercial activity started near 0 and now is growing substantially.

This chart compares six months ago Q3 2024, with Q1 2025. Here we can see for the first time we have line of sight to 50% commercial activity.

Here Gemini Q1 25 is ahead with 46% of users reporting using it for the ‘Shopping - Research’ commercial use case. Then we come down to 37%/34% for ‘Find’ and ‘Buy’ isn’t here yet as Gemini and ChatGPT don’t offer that yet. What maybe the biggest surprise is that the second commercial activity, by a long gap is vacation/travel at 14-16%.

There’s an important 'follow the data’ element here. Imagine you are a Product Manager at Google on the Gemini team and you are trying to win the war against ChatGPT, Meta and Perplexity. What’s the data telling you need to build to really delight customers? Yep, I am shocked we don’t have a Gemini fueled agentic shopping agent, but the week is still early ;-)

Use cases by age group

Commercial behavior is of particular interest to us, so let’s look at the age cohorts in Exhibit 8

In the research bucket, we see very strong growth across all cohorts. For comparison of prices we saw less activity - this is because Gemini really doesn’t encourage or enable price comparison, yet. The ‘Shopped for products’ bucket saw very strong growth in the 16-24 cohort.

Putting it all together

Looking at the funnel and marrying it together with the Morgan Stanley data we start to get a clear picture of where we are:

GenAI Usage - 175m US consumers, growing ~10% every 6 months and compounding quickly.

GenAI Commercial activity - 20-45% of that activity is commercial

GenAI Shopping - Research - Research leads commercial activity at 45% with Gemini really making big moves, but due to a lack of a shopping product, they stop.

GenAI Shopping - Find - 34-37% of that activity is find. ChatGPT just released their shopping cards in Q2, so that won’t be in the data yet, hopefully we see it in the next report.

GenAI Shopping - Buy - Sadly, only perplexity offers ‘true agentic’ shopping, so we’re at < 1% here so far.

Conclusion: Agentic Shopping is Spring Loaded

The data is clear, consumers are indicating with their intent and GenAI conversations, they are ready for agentic shopping. The real question is how fast can Meta, Gemini, ChatGPT, Apple and Anthropic in the US get there? Once they all have fully enabled from Research to find to buy agents, we’ll start to see some very interesting changes in online shopping.

If you missed it we covered in detail where each of the agents is in their build-out here.

It’s interesting to see the gap in the “Find” stage, especially since Gemini has already gotten this far but hasn’t really captured the “Buy” moment yet. Feels like the real inflection point might be hiding there.How do you see the product opportunities during this gap on your end?

Things are about to get exciting